Social Security:

Some facts and fiction

Recently, there have been

a variety of statements made about Social Security, many

negative, critical and downright scary.

Some are factual, but many are simply not true, especially the

fear-mongering ones. So we'd like

to take this opportunity to discuss a few in order to dispel the

myths and clarify the real situation about Social Security.

While we're at it, we'll add out opinions.

No. 1: Social

Security is Socialism.

This just plain is NOT true.

Socialism involves government ownership ol the means of

production. In other words, the people, via the government

own all businesses. Social Security is not a business.

It is also not social welfare.

It is a retirement

fund, one that is funded by payments made into the Social

Security Trust Fund (via FICA payments) by people who have jobs.

It appears to us that there is an

attempt to link Social Security with "social welfare"

which is erroneously also linked to "socialism," which

the general public often opposes (in some cases, without

actually knowing what socialism is). But Social

Security is neither.

To

read about Socialism, Capitalism and Communism

To

read about Socialism, Capitalism and Communism

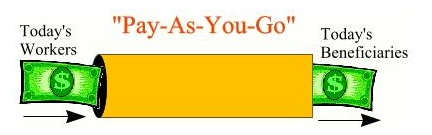

No. 2: Social

Security is a Ponzi Scheme.

Nope. It is a

pay-as-you-go system, one that also is used by some private pension

systems in the business world. It involves today's workers

contributing to the retirement (via income deductions) of those

who went before.

.

It has been noted that part

of the rationale for this arises from the fact that today's

workers create the work opportunities for tomorrow's workers,

and since they do that, when they reach retirement age it is

appropriate for those who are then working to contribute to

their retirement.

A superficial

comparison can be made between pyramid or Ponzi schemes and pay-as-you-go

programs in that both involve money from later participants going to

pay the benefits of earlier participants. But that is where the

similarity ends.

Social Security does not

require an increase in participants to pay for recipients.

Ponzi schemes do -- they rely on doubling of participants every

time a payment is made to a current beneficiary, or a geometric

increase in the number of participants. It is this

ultimately unsustainable requirement of people making payments

that causes all Ponzi Schemes eventually to fail.

Finally, with Social

Security, there does NOT have to be precisely the same number of

workers and beneficiaries at a given time--there just needs to

be a fairly stable relationship between the two. As long

as the amount of money coming in the front end of the pipe

maintains a rough balance with the money paid out, the system

can continue forever. There is no unsustainable progression

driving the mechanism of a pay-as-you-go pension system and so

it is not a pyramid or Ponzi scheme.

No. 3: Social

Security adds to the deficit.

Not True. Can't happen

under current law.

By law, Social Security funds

are separate from the budget, and it must pay its own way. That

means that Social Security can't add one penny to the deficit.

If Social Security income is insufficient to pay beneficiaries,

benefits may have to be reduced, but that's all.

Unless, of course, Congress

chooses to use general funds to pay Social Security benefits.

This could happen, but is not clear that it ever will happen.

But even were that to happen, whether it causes a "deficit" or

not will depend upon the income into the general fund (i.e.,

taxes) and the amount of other expenses for the general fund.

In other words, why and how a Federal Budget deficit occurs is

complication. So there are all sorts of things that can be

done in the Federal Budget that could make utilization of those

funds to pay Social Security irrelevant to any deficit.

We think that discussing the

federal deficit with regard to Social Security is far more

complicated than those who say it will happen (thereby

increasing the deficit) are willing to admit, or address.

In other words, we think it is simply a way to use a political

hot topic (the federal deficit) to critique and thereby justify

changing Social Security.

To

read about more about the Federal Budget

No. 4: Social

Security is going bankrupt

Ummm, no, it's not.

Even in the unlikely event

that nothing changes and the program's entire surplus runs out

in 2036, as projected, checks would keep coming. Payroll taxes

at current rates would cover 77 percent of all the future

benefits promised. That's true for young and old alike, and

includes inflation adjustments.

And up until 2023, Social

Security will be able to pay out all scheduled benefits without

any changes. Why? Because the reality is that by

2023, there will be a $4.3 trillion surplus in Social

Security .And after 2037, it could still pay out 75% of

scheduled benefits, without any changes. The program started

preparing for the Baby Boomers retirement decades ago.2

We think that those who

insist Social Security is broke are probably doing so, because

they want to break it themselves (like, maybe, privatize it).

No. 5: We have

to raise the retirement age because people are living longer.

There are two parts to

this: (a) assertion that people are living longer, and (b) the

assertion that this requires increasing the retirement age,

because it implies that each retiree is likely to draw more

money from Social Security than in the past.

But the first part is NOT

true, so the second part is invalid. People are NOT living

longer.

Follow along with us here,

because it gets a smidge complicated. The myth is based on

semantics, specifically the statement that "people are living

longer." Now, it is TRUE that the average life expectancy

has gone up. But you need to know that "average life expectancy"

is calculated FROM birth. In other words, it is a number

that says, on the average, how long people live FROM birth.

The reason that number has gone up is that fewer people die as

children than they did 70 years ago. AND, just so you

know, it is the case

that life expectancy from birth has only gone up around 2 years

for those at the bottom half of the income brackets, while those

at the top have gone up a little over 6 years.

Retirees are living about the same amount of time as they did 70

years ago. In other words, "life expectancy" from age of

retirement (around 65) hasn't gone up appreciably.

We think it is possible that those intent on cutting Social Security make

this false statement, because raising the retirement age is the

same as an across-the-board benefit cut.

No. 6:

People would be better off they kept their Social Security taxes

in their own private investment account.

Well, this really depends

on how much they could actually put in such an account.

And for most it would require faithfully putting that money

aside, every year of their working life, in a mix of stocks and

bonds, without ever skipping a year, drawing on their nest egg

or selling when the market dropped. AND it would depend on

whether, or not, those investments actually held value

(especially at retirement age).

Very probably easier said

than done. A person would need to invest far more than one

might expect to match the benefits Social Security pays. For

example, take a 65-year-old couple with a single breadwinner who

earned the average wage. At retirement, they'd currently get

about $2,170 a month, plus inflation adjustments, for life, the

Urban Institute reports. To equal that sum in private

savings, they'd need to have about $580,000, and the money might

last only 30 years.

We think this is simply a misleading assertion made by

those who want to privatize Social Security. We're not

mind readers, so we can say WHY they pitch for privatization,

but we do think that Wall Street and bankers could benefit, so

we wonder if that's not an underlying source for this idea.

No. 7: You

should get out of Social Security the amount you put in.

No. Social Security is not an

individual investment program (see Myth No. 6).

Current taxes (FICA) pay for

the earlier generation of retirees. Current workers are paying

for current retirees. The total amount of a person's benefit

depends on how much that earned, whether he, or she gets get a

spousal benefit, and age at retirement and how long the person

lives.

No. 8: The

Social Security Trust Fund has been raided and is full of IOUs

No, the Social Security Trust

Fund isn't full of IOUs.

It is full of U.S. Treasury Bonds. And those bonds are backed by

the full faith and credit of the United States.

It is full of U.S. Treasury Bonds. And those bonds are backed by

the full faith and credit of the United States.

The reason Social Security

holds only treasury bonds is the same reason many Americans do:

The federal government has never missed a single interest

payment on its debts. President Bush wanted to put Social

Security funds in the stock market--which would have been

disastrous--but luckily, he failed. So the trillions of dollars

in the Social Security Trust Fund, which are separate from the

regular budget, are as safe as can be.

It is true that buying those

Treasury Bonds put money into the general fund that belongs to

the Social Security Trust Fund, and paying it back to the Social

Security Trust Fund is part of the Federal Debt. BUT

remember that was money the Federal government used to pay for

other things, and that is the true source of possible deficit, not

the repayment of the bonds. Cutting taxes, while borrowing

to meet expenses has been a major contributor to deficits.

To

read about Equal Opportunity

To

go to the Articles Page